How Can You Give More?

Often the philanthropic are deterred by the idea that divesting themselves of some of their assets would impact, in an outsized way, themselves or their heirs through taxes. Again, this perception may or may not be true.

Unlocking their illiquid assets – real estate, personal property like copyrights and patents, and pension plans, business ownership – may help them achieve what they desire. They just need the know-how to get it done.

A Wealth Replacement Trust may be the solution.

A Wealth Replacement Trust combines three tools:

- A Charitable Remainder Trust (CRT)

- A life insurance policy, and

- An Irrevocable Life Insurance Trust

With these tools, a multi-level strategy is orchestrated to fulfill the donor’s wishes, benefit charity, and minimize the negative impact of unnecessarily paid taxes.

How does it work?

On the donor’s side:

The Process:

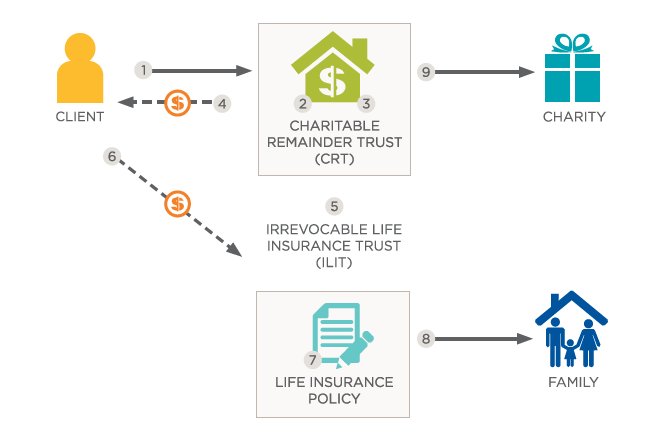

The donor irrevocably transfers highly appreciated property to a CRT

- The Trustee of the CRT sells the appreciated property and can receive the full fair market value (FMV) of the asset free of income taxes

- The Trustee then uses the proceeds of the sale to invest in income producing property

- The Trustee uses the income from the newly invested assets to pay the donor an income stream (annuity or unitrust amount) for life or for a term of up to 20 years

- The donor also establishes an irrevocable life insurance trust (ILIT) in which the donor has no interest or incidents of ownership

- The ILIT Trustee buys a life insurance policy on the donor’s life (or a second-to-die policy insuring both the donor and spouse) with death benefits equaling or exceeding the value of the property transferred to the CRT

- The donor uses the income received from the CRT each year to make gifts to the ILIT, which then uses the gifts to pay the life insurance premiums

For the Charity:

At the end of the CRT term, the remaining assets in the CRT are distributed to the designated charity, fulfilling the donor’s philanthropic goal.

For the Family:

At the donor’s death, the Trustee of the ILIT manages and distributes the tax-free death benefit proceeds according to the terms of the trust.

The Donor:

- Fulfills philanthropic intent to make a substantial charitable contribution

- Receives an immediate charitable deduction for the present value of the remainder interest going to the charity in the year the gift to the CRT is made

- Avoids capital gains taxes on the sale of the appreciated property

- Replaces all or a portion of the assets donated to the CRT with life insurance death benefit to his/her heirs

- Properly structured, the wealth replacement trust strategy removes the appreciated property and life insurance death benefit from the donor’s gross estate

The donor irrevocably transfers highly appreciated property to a Charitable Remainder Trust (CRT).

The Trustee of the CRT sells the appreciated property and can receive the full Fair Market Value (FMV) of the asset free of income taxes.

The Trustee then uses the proceeds of the sale to invest in income producing property.

The Trustee uses the income from the newly invested assets to pay the donor an income stream (annuity or unitrust amount) for life or for a term of up to 20 years.

The donor also establishes an Irrevocable Life Insurance Trust (ILIT) in which the donor has no interest or incidents of ownership.

The donor uses the income received from the CRT each year to make gifts to the ILIT, which then uses the gifts to pay the life insurance premiums.

The ILIT Trustee buys a life insurance policy on the donor’s life (or a second-to-die policy insuring both the donor and spouse) with death benefits equaling or exceeding the value of the property transferred to the CRT.

Upon the death of the donor, the ILIT distributes the tax-free death benefit proceeds to the donor’s heirs.

Upon the death of the donor or the expiration of the term of years, the assets remaining in the CRT is transferred to the charity named in the trust document.

The many moving parts of your estate – business, heirs, real estate, philanthropy, investments – need to be orchestrated in concert to maximize your legacy and reduce your loss to estate taxes. This requires significant inter-disciplinary expertise to realize the benefits and avoid the pitfalls. Planning Network Partners is dedicated to examining this and other opportunities as part of a larger picture of your whole financial health.

Contact Us today for expert assistance.